Fast Track to Shipping Decarbonization – Leaders Turn up the Heat

In the past month, there has been quite a lot of huffing and puffing around the need to kick start serious global shipping momentum towards decarbonization. The BIMCO CII Operations Clause for Time Charter Parties 2022 has come in for a good deal of criticism on account of widespread scepticism that charterers and owners will find the common ground to cooperate in the implementation. Equally, some owners have dismissed the whole concept of the Carbon Intensity Index on the grounds that it may actually result in higher emission levels – not less.

Against this background, the IMO Marine Environmental Protection Committee (MEPC) held its 79th session (MEPC 79) in London from 12-16 December 2022. Just to recap, the IMO’s GHG strategy makes express reference to the Paris Agreement, the key element of which is to reduce GHG emissions in sufficiently to hold the increase in the global average temperature to well below 2°C above pre-industrial levels while also pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels.

The IMO set out its ambitions in 2018 in its initial GHG strategy, targeting a 40% reduction in CO2 intensity by 2030, a 70% reduction by 2050, and a 50% reduction in all GHG by 2050, all with reference to 2008 levels. It would be fair to say that this strategy has failed to satisfy either side of the argument. There is a consensus among many large shipowners that the IMO strategy is weak and fails to address the scale of the problem. Many are therefore taking the bull by the horns and committing to a net zero target by 2050. Others believe the IMO strategy to be unrealistically ambitious.

Either way, there is considerable pressure on the IMO to set more ambitious targets, including from those who have already invested heavily in achieving net zero by 2050. Unfortunately, but predictably, MEPC 79 kicked the ball down the road to MEPC 80 in July 2023. Expectations for a fundamentally revised GHG reduction strategy will be high.

While global consensus building is taking place, the Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping (established in 2020) published a report in December 2022 detailing the key actions which in their view must be taken in order to fast-track decarbonization. The opinions of the Center matter, not just because of the size and experience of the parent company, but also because of the commitment of more than 50 influential partners spread over 18 nationalities that have committed to the initiative.

The Center’s report makes the following key points:

- International and domestic shipping uses approximately 12.6 Exajoules (EJ) of energy each year, corresponding to around 300 million tonnes of fossil fuels emitting more than 1 gigatonne of GHG emissions. To align with the Paris 1.5°C trajectory, the industry must limit its fossil fuel consumption of the global fleet to approximately 6 EJ by 2030. Several key levers were identified to fast-track the transition.

- Improving onboard energy efficiencyby just 8% – or 1% per year until 2030 – could save ~1 EJ of energy, equivalent to 24 million tonnes of fuel oil and 0.1 GtCO2eq of greenhouse gas emissions. To leverage this opportunity, shipowners and operators must take immediate action to increase energy efficiency in operation as well as by installing energy efficiency technologies in existing and new vessels.

- An array of energy efficiency measures and technologies and solutions are ready for use today such as voyage planning, weather routing, hull and propeller fouling management, air lubrication, propulsion-improving devices, engine technology, electrification, waste heat recovery as well as alternative power systems such as wind-assisted propulsion. However, most are lacking commercial incentives and regulation governing implementation which means their uptake to date is limited.

- The uptake of operational and technical energy efficiency measures varies across vessel categories and segments. There are some areas of growing application, particularly in the passenger, cruise, and container segments. In the fragmented bulk and tanker segments, although leading operators are applying energy efficiency measures, overall adoption remains low. As a result, the industry still has substantial potential to save onboard power, reduce energy consumption, and limit emissions.

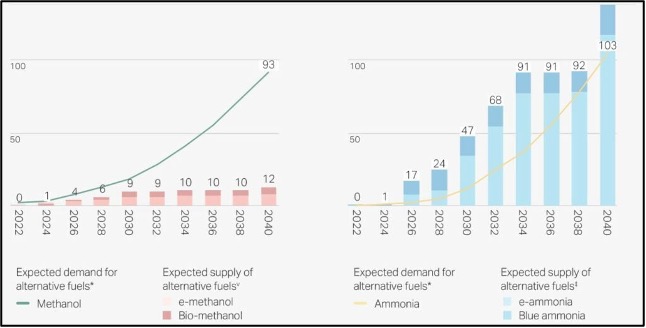

- The primary alternative future fuels include biomethane, e-methane, bio-methanol, e-methanol, blue ammonia, e-ammonia, bio-oils, and e-diesel.All alternatives face a degree of technical, safety, commercial, and regulatory challenges.

Source MAN Energy Solutions 2022

- The shipping industry is currently investing much more in alternative fuel technology and demand than fuel producers will be able to supply. This disconnect is partly because on-land investments in production infrastructure are much larger and riskier than investments in onboard technologies for alternative fuels. Current plans for alternative fuel production capacity suggest that supply will be unable to meet demand in the coming decades. It is estimated that this will result in a yearly shortfall of up to 20 million tonnes of alternative fuels. Furthermore, although the outlook indicates there will be a surplus of ammonia, methanol demand may outstrip supply by up to 80 million tonnes unless production is significantly stepped up.

- Long lead times mean we must start now to secure sufficient alternative fuel capacity to meet 2030 demand and beyond. To prepare to scale up alternative fuels, it is necessary to work on achieving technological readiness for all alternative fuel pathways and developing standards and regulations that ensure they are used safely, and with environmental and social responsibility. Another important point is addressing the imbalance between planned alternative fuel production supply and demand with solid investment commitments in large-scale fuel production infrastructure and building the competencies needed to scale up all alternative fuel pathways.

- The industry needs to develop regulations and measures that ensure alternative fuel pathways become commercially attractive. Emissions reduction and the uptake of new technology need to be incentivized through industry commitments and regulatory reform. Companies across the industry must set ambitious decarbonization targets and report their progress to create the traction and transparency needed to drive the transition forward. In this, it is critical to maintain a people-centered approach to ensure a safe and just transition.

As the main regulatory body, the IMO must focus on creating policies, targets, standards and regulations that drive the uptake of decarbonization technologies, eliminate uncertainty, and close the cost gap between fossil and alternative fuels. The report, details specific actions needed to be taken this decade including:

- Ambitious absolute emission targets from the IMO to reduce all GHG emissions from a well-to-wake perspective and reach net zero by 2050, aligned with the Paris 1.5°C trajectory.

- Supplementary emissions intensity and efficiency targets, intermediate targets for 2030 and 2040, global GHG pricing, and transparent emission reporting.

- Fast-tracked development of international rules and standards by the IMO to support alternative fuels and decarbonization technologies.

- Regional, national, and local policy roadmaps encouraging dedicated investments in green energy and fuel infrastructure for the maritime industry transition and engineering capacity to build these facilities.

- The speed of the transition will depend on how quickly first movers from across the supply chain can come together and demonstrate decarbonization solutions, business models, and best practices. However, being a first mover can be costly and uncertain. To support them in initiating the transition, first movers will require:

- Close collaboration across the value chain, between alternative fuel producers, ports, vessel owners/operators and cargo owners to demonstrate and prove technologies, business concepts, and standards/regulations, and share the learnings, challenges, opportunities, and best practices.

- Mobilizing regulatory, policy and financial bodies to help de-risk first mover investments and decarbonization activities.

- Wide support for first-mover initiatives that drive collective decarbonization and share costs, benefits, and risks, such as green corridors and Book & Claim systems.

The report concludes: “Decarbonization won’t happen overnight. We must prepare ourselves for decades of working together towards this common goal. We must change our mindsets from individualistic cost leadership to collaborative environmental leadership and we must start now. The future of our industry depends on it.”

Featured Image Courtesy: Maersk Line