Container Lines set for significant capacity expansion just as sailings are blanked

As the world’s major container ports gradually return to fluidity following more than two years of congestion during the Covid induced consumer spending spree, the container lines are again blanking sailings and laying up ships in order to manage capacity and support spot rates. The Ningbo Containerized Freight Index (NCFI) has been steadily falling in recent weeks and the rates to ship a 40’ units out of China are now hovering around the $10,000 level while Transatlantic rates are holding at around the $6,000 level.

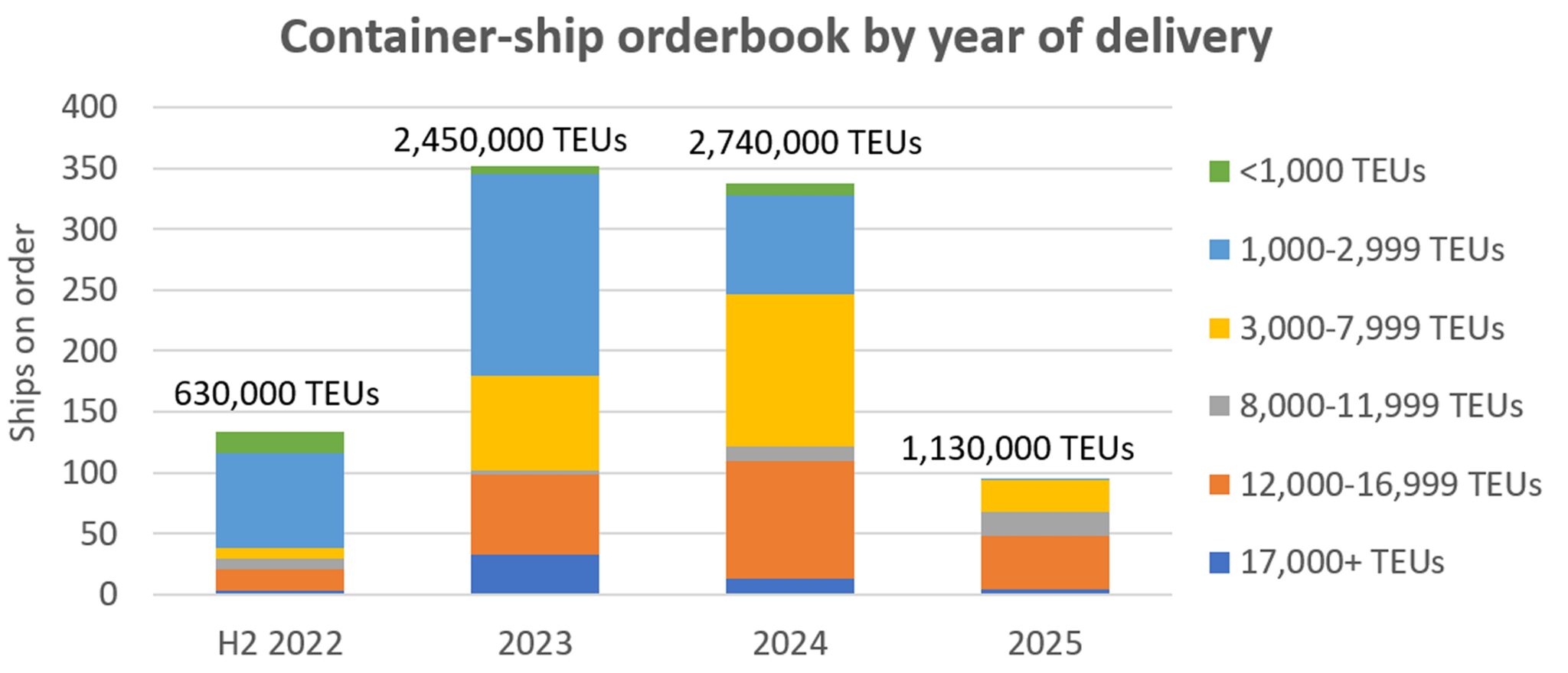

All this at a time when container vessel capacity on order from the shipyards is close to 30% of already deployed capacity. This can be compared to 8% just two years ago according to Alphaliner. In real terms this amounts to a staggering seven million TEU capacity increase equivalent to almost 300 of the largest container ships currently in existence. The mitigating argument is of course that the new vessels are required for fuel efficiency and in order to pave the way for new environmental standards as many older inefficient vessels are retired.

Inevitably, after a period of two years of outstanding profits, major owners are being enticed to invest in newbuilds, even at relatively high prices, in order to prepare for the next cycle of increased demand. This of course is dependent on geopolitical events including an end to the war in Ukraine, the taming of inflation, a return to real economic growth and avoiding another pandemic driven economic shut down. At the same time, many older inefficient vessels will likely find themselves operating a reduced speed or converted to razor blades next time round.

Beyond the container sector, the average age of the world fleet is increasing, standing at just over 12 years measured by weighted gross tonnage (up from a low of 9.7 years in 2013).

- Bulk carrier fleet average age 11.5 years (order book 7% of fleet capacity)

- Tanker fleet average age 12.1 years (order book 4.5%)

- Container fleet average age 14.2 years. (order book 30%)

- Around 28% of the total global tonnage is aged over 15 years.

Uncertainty over future propulsion technology and risk continues to constrain fleet growth and the speed of decarbonisation. Clarksons predicts that:

- Total newbuild orders will increase from $64bn (2016-2020) to $139bn a year (2021-2030).

- $1.4 trillion of newbuild orders are needed for fleet renewal 2021-2030 and $4.2 trillion through 2050).

In terms of the fourth propulsion revolution, operating efficiency and the race to develop alternative fuels, Clarksons reported last month that there are now 320 LNG ready vessels in service along with 100 LNG ready, 130 ammonia ready and 6 hydrogen ready on order. LNG and other alternative fuels make up 4.5% of the fleet when looking at the gross tonnage, 44% of the orderbook and comprise 59% of all newbuild orders by tonnage. Breaking down the orderbook:

- 9% of tonnage is set to use LNG (781 units)

- 2% to use LPG (86 units)

- 3% due to use other alternative fuels (260 units; including methanol (42), ethane (11), biofuels (5), hydrogen (12) and battery/hybrid propulsion (200).

Chart: American Shipper based on data from Clarksons Platou Securities. Note: additional 50,000 TEUs is on order for 2026 delivery

Equally important for those who enjoy the statistics, while the installation of Exhaust Gas Cleaning Systems (scrubbers) has slowed down, systems are now fitted to almost 5000 ships (including those pending retrofit), equivalent to around 25% of total gross tonnage. This is being further driven by the steady fuel price differential between HSFO and VLSFO of $200-300 per tonne.

It was also reported that:

- The number of ports providing LNG bunkering is around 150 and is expected to be 250 by 2026.

- Modern so called eco vessels now form about 30% of the fleet by gross tonnage resulting in recalculation of asset values and charter market earning potential.

- Shipping emissions are down by 17% since 2008, driven in part by a reduction in speed of about 20% (container ships 25%) and design innovations. At the same time, moving 40% more cargo is moving in 90% more ships.

- Energy-saving technologies have been fitted on over 5,550 ships, accounting for 24.5% of fleet tonnage. The technologies employed include, Flettner rotors, wind kites, propeller ducts, rudder bulbs and air lubrication systems.

- Shipping remains the most “carbon efficient” mode of transport (x3 rail and x11 truck).

- Just over 70% of the fleet is now Ballast Water Management System fitted.

- To ensure accurate comparisons, industry bodies are urging for a well-to-wake approach to calculating emissions of alternative fuels as a way of ensuring overall emissions reduction targets are achieved.

It is encouraging that regardless of politics and fragmented legislation, industry research and debate to establish a preferred fuel for the future is gaining momentum. Let us hope that the huge investments being made by the container lines in fleet renewal do not result in financial stresses that hinder progress.

Feature Image Courtesy: Robban Assafina